")

Welcome back to the Admin Partners Blog! Let’s take a dive into the proposed Secure 2.0. As a reminder, this bill now goes to the Senate where we expect to see changes. It will then go back to the House (with Senate changes for another vote) before it would get to the President for signature. There are several other important pieces of legislation in the Senate that will likely be addressed before this gets worked on. So, while there is a lot to unpack in this legislation, there is plenty of time to further understand the proposed changes.

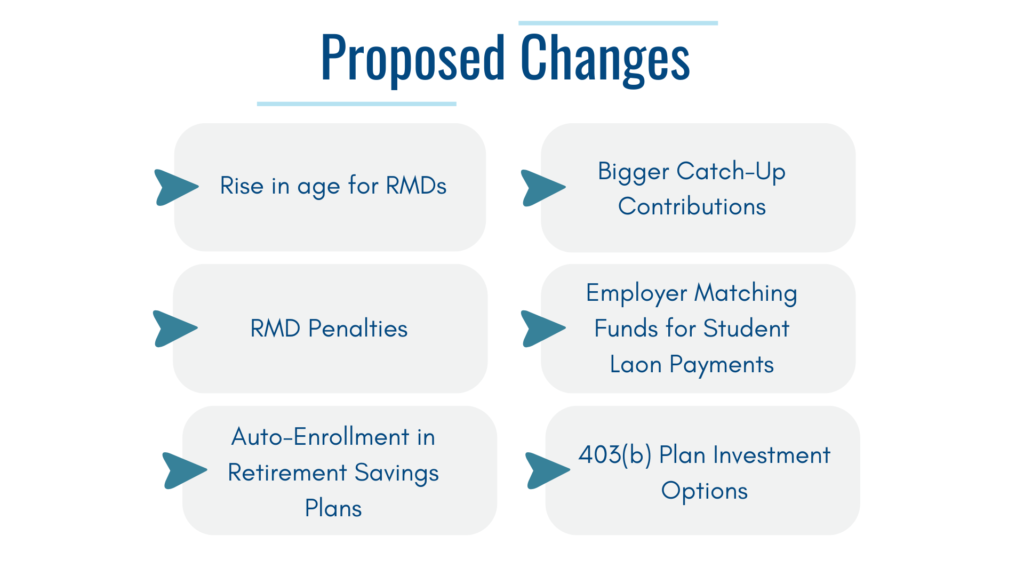

Here are some of the proposed changes.

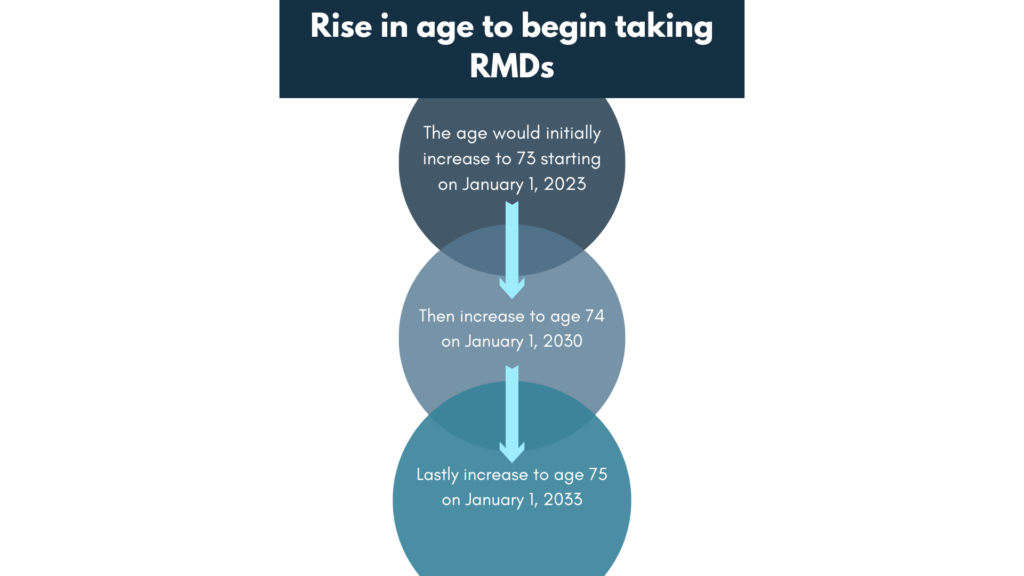

Rise in age to begin taking RMDs

SECURE 2.0 would again raise the age to begin taking RMDs, this time to age 75 over a decade. The age for RMDs would initially increase to 73 starting on January 1, 2023, then to age 74 on January 1, 2030. It would rise to 75 on January 1, 2033.

RMD Penalties

Currently, if you fail to take your full RMD, the shortfall is hit with a 50% excise tax. That’s one of the harshest penalties you can face from Uncle Sam. However, under SECURE 2.0, this would be reduced to 25%. If the mistake is corrected in a timely manner, the penalty would be further reduced to 10%.

Auto-Enrollment in Retirement Savings Plans

SECURE 2.0 would require employers to automatically enroll eligible workers into the firm’s 401(k) or 403(b) plans at a savings rate of 3% of salary – although workers would be able to opt out or opt to save less or even more, up to annual contribution limits. Additionally enrolled workers’ contribution rates would automatically increase each year by 1% until their contribution reaches 10%.

Businesses with fewer than 10 employees, businesses which opened fewer than three years ago and retirement plans for churches and government agencies would be exempt. Additionally, businesses with 401(k) or 403(b) plans in place before the enactment of SECURE 2.0 would be exempt.

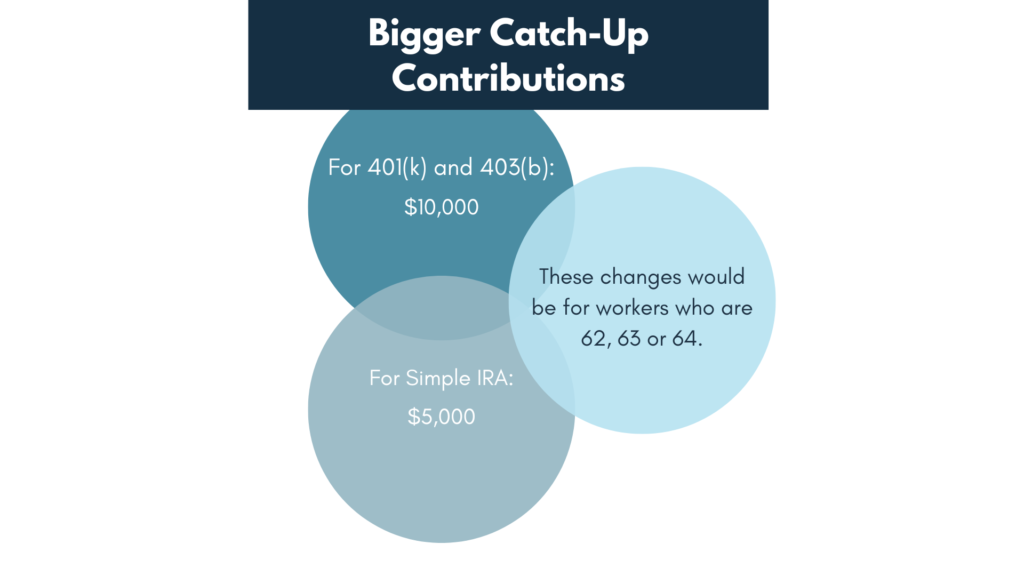

Bigger Catch-Up Contributions

Currently, workers who are at least 50 years old can make catch-up contributions to their retirement accounts above the normal pay-in limits. For 2022, these workers can contribute an extra $6,500 to 401(k) and 403(b) plans after hitting this year’s $20,500 limit. For a SIMPLE IRA, they can add $3,000 more to the $14,000 cap in 2022.

Under SECURE 2.0, workers who are age 62, 63 or 64 would be able to contribute even more to these accounts. For 401(k) and 403(b) plans, these employees would be able to make up to $10,000 in catch-up contributions, while participants in a SIMPLE IRA could put in up to $5,000 in catch-up contributions. Both of these limits would be indexed for inflation each year.

Employer Matching Funds for Student Loan Payments

Traditionally, employers match participants’ contributions to their retirement accounts. But some workers may be unable to fund their retirement account as they prioritize paying down student loans. The proposed legislation would allow employers to make matching contributions to a worker’s retirement account based on the worker’s own student loan payments. This would apply to 401(k) plans, 403(b) plans, SIMPLE IRAs and 457(b) plans.

403(b) Plan Investment Options

Currently, 403(b) plans can generally only invest in annuity contracts and mutual funds, preventing participants from investing in collective investment trusts. A collective investment trust is a group of pooled accounts. This lowers fees by achieving economies of scale.

SECURE 2.0 would allow 403(b) custodial accounts to invest in collective investment trusts, if certain conditions are met, including that the plan is subject to the Employee Retirement Income Security Act of 1974 (ERISA) and the sponsor accepts fiduciary responsibility for selecting the investments participants can choose from.

Those are some highlights in the proposed legislation, please stay tuned for upcoming updates! We will keep everyone informed as this bill moves through the Senate.